DFID recently launched its ‘International Development Infrastructure Commission’ which aims to ‘turbo-charge quality infrastructure projects in developing countries.’ Petter Matthews, EAP Executive Director and International Chair of the Civil 20 (C20) Infrastructure Working Group, reflects on the focus of the Commission and cautions that its scope is too narrowly defined.

UK Secretary of State for International Development Alok Sharma is from a corporate finance background and it appears that he has drawn on his old address book when appointing members of the International Development Infrastructure Commission (IDIC). This isn’t surprising given that the focus of the Commission is to ‘help make investment in infrastructure in developing countries more attractive to businesses and investors’. Whilst it’s positive that the Secretary of State recognises the importance of infrastructure, I have two concerns with this emphasis.

First, it is unrealistic to think that this ‘private finance first’ approach will close the infrastructure gap, particularly in low-income countries (LICs) which are characterised by weak institutions. Secondly, a narrow focus on mobilising additional finance could distract attention from other solutions that are particularly import in LICs. I’ll examine each of these concerns.

Challenging private finance first

The G20 and the multilateral development banks have championed the mobilisation of private finance through the establishment of infrastructure as an asset class. This involves converting

investments into standardised financial instruments that are easy to buy and sell and provide a reliable revenue stream for investors. These developments, it is envisaged, will unlock private investment and help close the infrastructure gap. However, the amount of private investment currently going into LICs is miniscule and there are good reasons for this.

Infrastructure investments in LICs are often risky and unprofitable, particularly those most likely to leave no-one behind such as rural roads, urban sanitation and primary health care facilities. Investments in other sectors, such as telecoms, urban transport and energy, can in theory be de-risked to make them more attractive to private investors, but this usually means transferring that risk to the public sector in the form of contingent liabilities. There are numerous examples of failed investments where governments have been forced to bailout investors with serious consequences for the public purse.

These challenges help explain why public finance remains by far the most important source of investment in low and middle-income countries. The Asian Development Bank for example points out that in Asia as a whole, the public sector provides 92% of infrastructure investment. Recognition of this has led critics of the private finance first approach to argue that this focus on private financing is distracting attention from the most important challenge, i.e. improving the quantity and quality of public investment.

There is a compelling logic to this argument. It seems a more realistic prospect to close the infrastructure gap through a relatively modest increase in public investment, than it is through an exponential increase in private finance. This is particularly true when the savings can be made through reducing inefficiency in public investment that are on average forty per cent in LICs.

Beyond financing

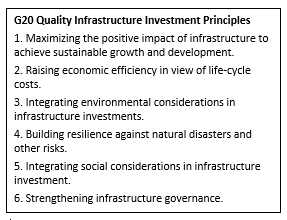

The G20, under Japanese leadership in 2019, has shifted its focus beyond financing through its adoption of the Principles for Quality Infrastructure Investment (QII). Finance remains integral,  but alongside it is a range if issues that are also considered essential to close the infrastructure gap.

but alongside it is a range if issues that are also considered essential to close the infrastructure gap.

This shift draws on the experience of the Japanese Government which itself has a history of strong public involvement in the provision of infrastructure. I hope the IDIC will consider the QII Principles and the people-centred proposals put forward by the C20. These include:

Governance – Probably the single greatest opportunity to close the infrastructure gap, improving governance helps to reduce inefficiency, strengthen public institutions and build trust. Its importance was captured succinctly by the former CEO of the Global Infrastructure Hub Chris Heathcote: “There’s a growing realisation . . . that if you get the governance aspects right, the finance will follow. Get it wrong and the investment will dry up.”

Transparency and accountability – On average, forty per cent of investments in LICs are lost through corruption, mismanagement and inefficiency. Reducing these losses could result in up to forty per cent additional productive investment, without having to mobilise additional finance. Improvements in transparency and accountability are key to meeting this challenge.

Inclusion – All people should benefit from the design, construction, operation and maintenance of infrastructure. However, this will not occur without purposeful consideration of inclusive approaches that for example: support meaningful stakeholder engagement, promote women’s economic empowerment, incorporate universal design for disability inclusion, integrate safeguarding mechanisms, promote safety in public spaces and reduce gender-based violence.

Labour standards – Construction is a good source of employment in LICs, but too often jobs are informal, poorly paid and workers are subject to a high-risk of injury, disease and even death. Workers’ rights are best protected through ratifying and effectively implementing relevant international labour standards related to construction and through strong trade unions and collective bargaining.

No silver bullets

Private financing is not a silver bullet to close the infrastructure gap. If the IDIC is to really help turbo-charge quality infrastructure projects, it should consider strengthening public investment and a range of other issues that are also essential to ‘leaving no one behind’.

DFID itself provides a deep well of experience to draw from in this regard. It has a good track record of building governance capacity, strengthening institutions and improving transparency and accountability. It also has a cadre of infrastructure advisers who understand the complex challenges involved and demonstrate commitment to delivering comprehensive solutions. It is hoped that the IDIC will draw on their experience and that of civil society organisations, in addition to the financiers, when formulating its recommendations.